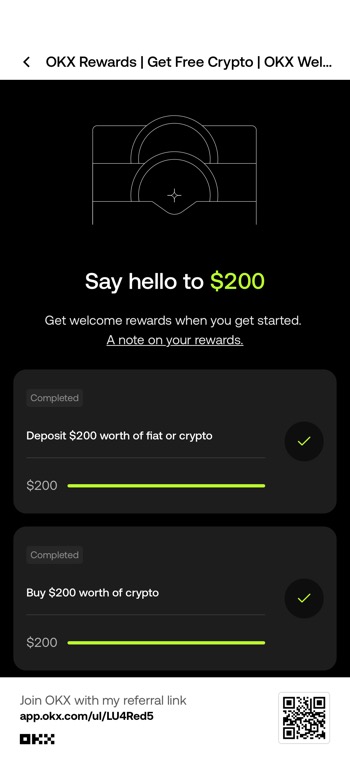

Update December 2025: SoFi announced some changes to their available features and what is only available with their SoFi Plus “Premium” membership program. I feel that they are trying to build something like “Robinhood Gold”, but hopefully better promos are coming because I don’t feel the perks are worth the cost right now. First, there are now three different ways to earn their higher APY tier (any single ONE of these is enough):

- Eligible Direct Deposit of any amount (even $1). Many people can split their paycheck multiple ways.

- $5,000+ in combined balances across SoFi Checking and Savings accounts

- SoFi Plus members that pay $10/month fee.

You can see this on their rate sheet (as of 11/12/25):

Second, SoFi Plus is now paid-only at $10/month. You no longer get it for free with a direct deposit, although they are extending complimentary access to all SoFi Plus benefits through March 30, 2026 with eligible deposits. You can see a list of SoFi Plus benefits here.

For the most part, the SoFi Plus benefits are the same as before. A notable new addition is the SoFi Smart Card which is a charge card linked to your SoFI Bank accounts that offers unlimited 5% cash back at grocery stores.

Otherwise, I would say the most valuable SoFi Plus perks that existing Direct Deposit folks lost with this change are:

- 10% rewards boost on the SoFi Unlimited 2% Credit Card, which turns the 2% cash back into 2.2% cash back.

- 2% match on recurring IRA contributions, plus a 1% match on recurring deposits made through SoFi Invest taxable brokerage accounts.

- Possibly the ability to “schedule an unlimited number of appointments with a financial planner”, although I’m not sure of the quality of this advice. There is no indication you’re guaranteed at least a CFP. I’ve never used this feature, but it might be nice if you wanted to get some general advice.

Update April 2024: SoFi made a few notable changes recently, both positive and negative:

- The SoFi Unlimited 2% Credit Card added 10% boost on their rewards with direct deposit into SoFi Checking or Savings. This would work out to 2.2% cash back rewards points on everyday purchases. (As of December 2025, this is now restricted to SoFi Plus members paying $10 a month.)

- There is a new inactivity fee of $25 per account for every 6 months of login inactivity.

- The outgoing ACAT transfer fee was increased to $100. Previously $75.

Original post:

SoFi (“Social Finance”) is an all-in-one finance app that expanded from students loans into banking, stocks, crypto, credit cards, and more. Here are their current promotional offers; New users can receive a separate opening bonus for each separate part of SoFi (Money, Invest, Loans, etc).

- SoFi Checking Referral Offer: Up to $325 new user bonus. Open a new SoFi Money account and add at least $10 to your account within 5 days, and get $25. Then get up to $300 additional bonus with qualifying direct deposit. Plus up to 4.30% APY.

- SoFi Credit Score Tracking Offer: $10 in rewards bonus points. You’ll earn $10 in rewards points when you activate free credit score monitoring

- SoFi Invest Referral Offer: $25 new user bonus. Taxable brokerage account. Open an Active Investing account with $10 or more, and you’ll get $25 in stock.

- SoFi 401(k) Rollover Offer: Up to $10,000 Bonus. Get a 1% match when you roll over your 401(k) into a SoFi IRA. Partnered with Capitalize to make the transition easier.

- SoFi Student Loan Refi: $300 bonus. Warning: Do your research before refinancing your Federal student loans to a private lender.

- SoFi Doctors and Dentists Student Loan Refi: $1,000 bonus. Special low rates just for doctors and dentists.

- SoFi Private Student Loan: $300 bonus.

- SoFi Personal Loans Referral Offer: Fixed $300 bonus. Fixed $300 bonus, 90 days after successful funding. The loan has no fees and you can pay it back in full after 90 days (you can pay it down to $50 before then to accrue minimal interest, thus making a new profit after the bonus).

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)