Barclays Bank Delaware is an FDIC-insured US bank with a limited-time offer of a $200 bonus if you deposit $30,000+ in new funds into their Tiered Savings Account. You must fund within 30 days of opening, and maintain the balance of at least $30,000 for another 120 consecutive days after funding. Bonus arrives after another 60 days. You must be a new Barclays Tiered Savings customer (current and previous Barclays customers with a Savings or CD are not eligible). Note that they have other flavors of savings accounts, so be sure to apply for the right one. Direct deposit is not required. Offer expires 12/31/2025.

There is a slightly better version of this bonus for AARP members (you will need an active membership number).

Here are the current interest rate tiers, as of 10/19/25. Note that it’s basically a 3.90% APY account unless you have a $250,000 balance. As with all savings accounts, the rates are also subject to change at any time.

Bonus math. This is a 0.66% bonus on $25,000 if you keep it there for 120 days, which makes it the equivalent of 2% APY annualized. Bonus will be paid around Day 180 and the account must be open at that time, but you only need to maintain full balance through Day 120 after funding. The bonus is on top of the standard interest rate, currently a relatively competitive 3.90% APY for a $25,000 balance as of 10/19/25.

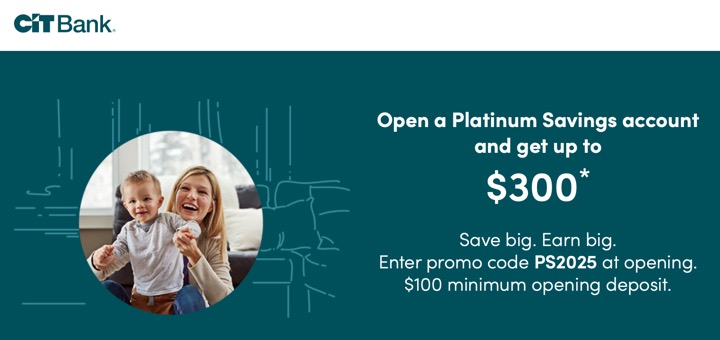

The equivalent of roughly 5.90% total APY over 120 days makes it a decent offer for those with compatible balances looking for short-term place to hold their cash for a few months. However, it’s not as good as the currently live CIT Bank deposit offer that offers $225 for $25k and $300 for $50k with no minimum holding period.

Activation reminder for 2025 4th Quarter. The credit cards below offer 5% cash back and up on specific categories that rotate each quarter. It takes a little extra attention, but it can add up to hundreds of dollars in additional rewards per year without changing your spending habits. You can also buy gift cards for other retailers at places like Grocery Stores and Home Improvement stores with 5% back now but spend the gift cards later. New cardmembers may also get an upfront sign-up bonus.

Activation reminder for 2025 4th Quarter. The credit cards below offer 5% cash back and up on specific categories that rotate each quarter. It takes a little extra attention, but it can add up to hundreds of dollars in additional rewards per year without changing your spending habits. You can also buy gift cards for other retailers at places like Grocery Stores and Home Improvement stores with 5% back now but spend the gift cards later. New cardmembers may also get an upfront sign-up bonus.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)