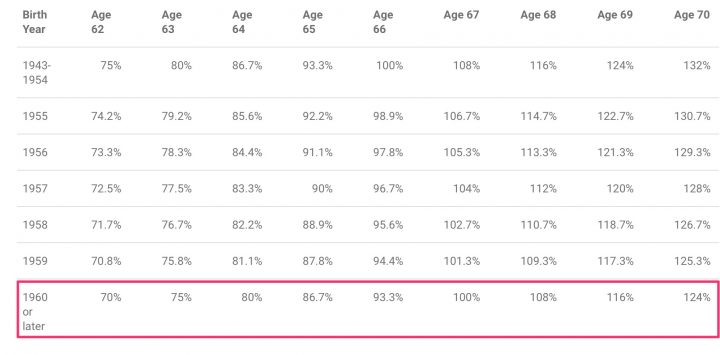

An important choice in retirement planning is when to start claiming your Social Security benefits. If you claim earlier, your monthly benefits will be reduced for the rest of your life. If you claim later, your monthly benefits will be increased for the rest of your life. Here is how much of the benefit taken at “full retirement age” will change based on your birth year. Taken from Fool.com using data from SSA.gov. Found via Early Retirement Forums.

This can be a complicated question, but if you were to force a rule of thumb*, it would probably be to wait to claim as late as you can in order to maximize your total lifetime benefits. (* Don’t just follow this blindly. There are many online calculators to help you with the details, especially for couples, like the free Open Social Security.)

Social Security is the only place you can “buy” a lifetime of guaranteed inflation-adjusted income. The difficulty is that you have to “buy” it by living off your other investments until your claim age.

Here are some interesting charts from the article The Retirement Solution Hiding in Plain Sight: How Much Retirees Would Gain by Improving Social Security Decisions, which analyzed the “actual Social Security decision and wealth accumulation of 2,024 households in a Social Security Administration sponsored panel survey.”

As you can see, the optimal claim age to maximize total lifetime benefits is mostly tilted towards the maximum age of 70. However, the actual claim age is heavily clustered towards the earliest possible age of 62.

How much difference are we talking about? Here is a chart showing of the average lifetime increase in income if you went for the optimal instead of the actual (in percentages).

In a recent

In a recent

Here’s my 2023 Q2 income update for my

Here’s my 2023 Q2 income update for my

One of the concerns about contributing to 529 plan for college savings is that you won’t end up using all the money and end up being hit with additional taxes (at ordinary income rates) and penalties on an non-qualified withdrawal. The funds potentially would have been better off simply invested in a taxable brokerage account (and long-term capital gains rates).

One of the concerns about contributing to 529 plan for college savings is that you won’t end up using all the money and end up being hit with additional taxes (at ordinary income rates) and penalties on an non-qualified withdrawal. The funds potentially would have been better off simply invested in a taxable brokerage account (and long-term capital gains rates).  Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.  The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)