I’ve been traveling internationally for the last couple of weeks, and with all the chaos of trying not to lose any of the kids on whatever multi-transfer subway ride or hiking trail is on the agenda every day, I felt quite relieved that my finances were so low-maintenance. Buy-and-hold means I don’t need to check stock market quotes, I pay all my bills online once a month for 10 minutes, and I have enough cash cushion so I don’t stress about daily cashflow (matching up payday timing with expenses).

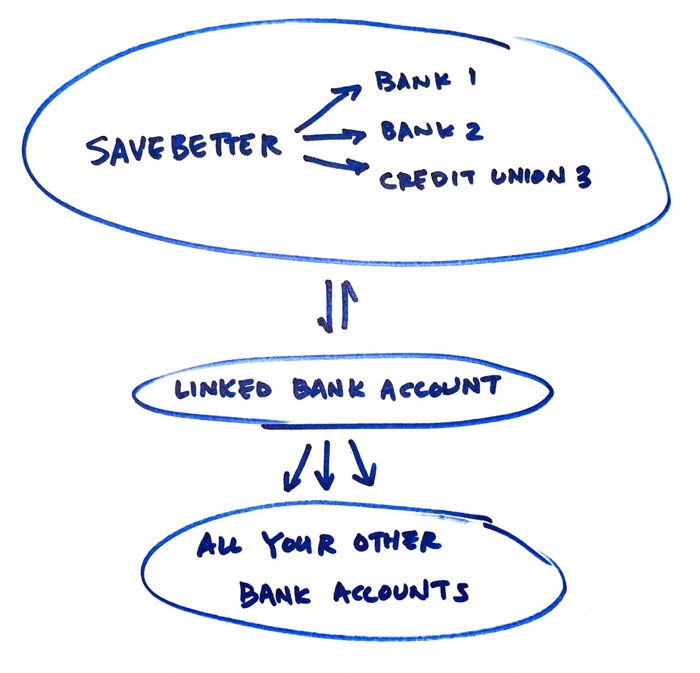

Unfortunately, for the folks that put their day-to-day cash in the “checking accounts” of fintechs like Juno and Yotta, the past few weeks have been the opposite. Their cash is frozen in limbo, with a bankrupt Synapse (Banking-as-a-Service provider) rapidly winding down and shedding all of their employees while pointing the fingers at everyone else.

Roughly $85 million in user deposits is unaccounted for. The ledger of transactions and balances does not match up between Synapse and Evolve. The bankruptcy judge apparently has very little power (and no money) and has resorted to asking for a private forensic accounting firm to help out “pro bono”. Given the possibility of theft there, I think potential jail time should be on the table, personally. Jason Mikula of Fintech Business Weekly is still the best source track new developments.

To be clear, the users of Yotta and Juno had ABA routing numbers and account numbers from Evolve Trust & Bank. Users could very well be forgiven for assuming that they had “direct” or demand deposit accounts (DDA) accounts at Evolve Trust & Bank.

The FDIC has maintained their stance that this is not a bank failure, and thus not their responsibility to help. Instead, they just quietly updated their website with some “helpful” Consumer News:

Increasingly, some consumers are choosing to open accounts through nonbank companies (typically online or through mobile apps), such as technology companies providing financial services (often referred to as fintech companies), that may or may not have business relationships with banks. If and how a bank is involved is key to understanding whether or not your money is protected by deposit insurance. However, in some cases, it is not always clear to consumers if they are dealing directly with an FDIC-insured bank or with a nonbank company.

[…] However, FDIC deposit insurance does not protect against the insolvency or bankruptcy of a nonbank company. In such cases, while consumers may be able to recover some or all of their funds through an insolvency or bankruptcy proceeding, often handled by a court, such recovery may take some time. As a result, you may want to be particularly careful about where you place your funds, especially money that you rely on to meet your regular day-to-day living expenses.

This is clearly a huge regulatory blind spot. The FDIC (along with other regulators) has publicly allowed millions of individuals to open up accounts at this companies which promote “banking” services, “savings accounts”, “checking accounts”, and most importantly ‘FDIC-insurance”. The FDIC has allowed this advertising to happen for years and years. Everyday consumers clearly believed that their money is “safe” and FDIC-insured. Why wouldn’t they? The system benefited from the addition of billions of dollars in deposits into partner banks. Many of these customers are the previously “unbanked” and “underbanked”.

Chime has over 20 million customers and over $6 billion in deposits. You think all those people know that they could instantly lose access to their money for months? You think they know they could experience permanent financial loss if Chime doesn’t track everything perfectly?

I truly believed that some regulatory agency, perhaps the Consumer Financial Protection Bureau (CFPB) in collaboration with the FDIC, would step in to close up this blind spot. The Federal Trade Commission. The Federal Reserve. But instead, everyone has backed away. In my opinion, this is a case of many small individual consumers being ignored. If this was a bigger story, if there was more political pressure from a single powerful person or company, I believe some positive action would have occurred.

Instead, fintechs are essentially sent back to the age of the Great Depression, before there was FDIC insurance and you never knew if your bank would fail and your money would disappear. How is the individual consumer supposed to know if their fintech is properly reconciling every single transaction? If a company can simply lose $85 million of user deposits that were marketed as “checking accounts” with “FDIC insurance” and not have any repercussions because they declared bankruptcy, then this is the Wild West again. What does it matter if pass-through FDIC insurance exists, if a simple addition or subtraction reconciliation error from the company can negate it?

The following quote is credited to John Maynard Keynes when questioned about changing his stance (long backstory):

When the facts change, I change my mind – what do you do, sir?

Well, I’ve changed my mind. The FDIC has allowed misleading marketing for years, all while the member banks have profited from fintech deposits. Yet it won’t protect the affected everyday consumer. I will no longer trust any fintech with my money for longer than it takes to grab a quick sign-up bonus. I’ll probably avoid any sort of deposit bonus that requires a longer hold period. In my opinion, even the silence from other fintechs has been disappointing. This event stains them all. I will no longer maintain any significant balance at a fintech.

Dig deeper into the weeds here, here, and here.

Photo by Jeremy Bishop on Unsplash

Juno.finance (formerly OnJuno) is a fintech that combines an FDIC-insured bank account and a crypto custodian. Details:

Juno.finance (formerly OnJuno) is a fintech that combines an FDIC-insured bank account and a crypto custodian. Details:

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)